Your pension pot probably isn’t enough - the pensions industry admits it

You have to act on your own contributions as early as you can if you want to have more money to fund your epic retirement.

In this week’s newsletter:

Feature: Your pension pot probably isn’t enough - the pensions industry admits it

From Bec’s Desk: Another week in the UK

Your pension pot probably isn’t enough - the pensions industry admits it

I’ve spent the week immersed in the world of UK pensions at the enormous Pensions UK conference - the biggest pensions conference in the UK - listening to policymakers, fund managers and advisers talk honestly about the state of the system. The message was loud and clear: reform is coming but not soon enough for today’s retirees. Everyday people will need to take charge of their own future if they want a better retirement because the government is unlikely to drive change that will help today’s retiring generation.

Behind the polished speeches, there’s deep frustration and even cynicism. Many industry insiders have already withdrawn their 25 per cent tax-free lump sums, fearing what might change in the next Budget. Others are holding off, hoping the government will deliver badly-needed long-term stability.

The shift from defined benefit (DB) to defined contribution (DC) pensions – where your retirement income depends on how much you save and how your investments perform - is well underway. The problem for today’s and tomorrows retirees? Most DC pots are too small to provide a sizeable income. With only 8 per cent in combined contributions (from you and your employer), too many people will reach retirement with nowhere near enough. And with one in five Britons nearing retirement, that’s a big problem for the economy and for families.

What’s really worrying the experts

Let’s talk about it… because this stuff combines into some decent issues.

The State Pension.

The triple lock – which guarantees annual increases by the highest of inflation, earnings or 2.5 per cent – has been brilliant for retirees, but it’s expensive for the government. Many insiders fear it’s unsustainable without stronger growth or higher taxes. Any attempt to change it could become politically explosive. It could mean lower effective state pensions, and more need to save to fund your own retirement in the UK.

The public funding of government pensions.

Unlike countries such as Australia, the UK doesn’t have a sovereign wealth fund set aside to help pay for government and public sector pensions. Instead, the bill for those defined benefit promises lands squarely on today’s taxpayers. Some in the industry even joke that it’s “the great British Ponzi scheme” – the young paying for the old.

Plenty of experts would love to see the UK invest in a national fund to secure the future of these obligations – something that could help stabilise the system for generations to come. The trouble is, no one can quite see how the government could afford to do it right now. Watch this space.

The contribution gap.

Everyone agrees: 8 per cent contributions to UK pensions simply isn’t enough to fund a comfortable retirement, even over the long term. The industry consensus is clear – contributions need to march gradually towards 12 or even 15 per cent so workers and employers can adapt without too much pain. The maths is straightforward: higher contributions today mean more comfortable retirements tomorrow, thanks to the power of compounding.

But the Minister for Pensions, Torsten Bell MP, admitted this week that the government can’t afford to make that shift right now. Perhaps the new Pensions Commission could take it out of the political spotlight and make a bold, independent recommendation – but even then, someone will have to act. Because the harsh truth is this: if you coast through your working years on the minimum contribution, you’ll likely reach your fifties or sixties only to realise it’s too late to catch up.

So here’s what I want you to hear: you can’t wait for the system to fix this. You have to act on your own contributions as early as you can if you want to have more money to fund your epic retirement.

The good news: some practical fixes are coming

1. Guided retirement pathways.

Too many people are scared to even open their pension app because they know they don’t have a lot and they don’t understand what to do with it. The government is pushing for funds to provide “default retirement journeys” - simple, guided drawdown options that help you turn your pension into income without running out of money before you die. Funds are working hard on this, and in the next 1-2 years some helpful offerings will evolve.

2. Bigger, better funds.

The UK has thousands of small, inefficient schemes. Consolidation into larger “megafunds” should reduce costs of most pensions and improve the investment returns - if done transparently.

3. Real value for money.

A major win for consumers is the new Value for Money framework which is being worked through by the industry. Soon, you’ll be able to see exactly how your fund performs, what fees you’re paying and whether you’re getting good returns. Transparency has long been missing in the UK system – but it’s finally on the way. And I’m going to watch this space with you.

What this means for you

Reform will take years, not months. But here’s what you can do now:

Check your contributions. If you’re only paying the minimum 8 per cent, see if you can bump it up – even a little. A few extra pounds each month might not feel like much now, but over decades it compounds into real money. And don’t forget the best bit: tax relief means the government chips in too, so every pound you add actually costs you less than you think.

Know your investments. Ask your provider what your default fund is and how it’s performing. Be alert to your ability to get good returns on your investments, and stay invested in growth assets. Ask your fund what age your lifestyle option is set for you to retire at - if it’s not aligned with your planned retirement age, you might find you’re being adjusted out of growth assets too early.

Plan your drawdown. Don’t wait until you leave work to figure out how your pension becomes income. Learn about it.

Start thinking about which pot deserves to be your main one. If you’ve got a handful of old workplace pensions scattered across different providers - which most people do as they start to prepare for retirement – it’s time to take a closer look. Compare which one has the best long-term returns, lowest fees, and the clearest tools or support to help you plan your retirement income? That’s probably the one to keep and build on.

Merging your smaller pots into a strong, well-performing fund can make your money work harder and make life simpler down the track. Just check before you move anything – It can be tricky to review, and some older schemes offer guarantees or benefits you don’t want to lose.

Stay engaged. The people inside the system know that 8 per cent and autopilot won’t get you there. Stay engaged with your pension - use the tools your provider offers to learn and get the best outcome you can.

The big takeaway from Pensions UK?

The UK pensions system is waking up to the needs of today’s pre-retirees – but you’ll retire better if you do too.

Hey everyone,

A short one today. I’m back in Australia after two jam-packed weeks in the UK — full of brilliant conversations about the future of pensions and retirement. I met so many smart, passionate people across London and Manchester who are determined to make the UK system work better for everyday savers. I came home inspired (and maybe just a little jet-lagged).

While I was there I met up with some of our UK moderators of The Epic Retirement Club Facebook Group too - a fabulous day (and I wish I took more photos). And I presented on the enormous engagement with Epic Retirement on the stage too. I also got to spend time with teams from almost all the big UK pension funds.

Over the next few months, I’ll be sharing more insights from those conversations and more – including what’s changing with the new Pensions Commission, what it might mean for contribution rates, and how you can take charge of your own pension and retirement planning now rather than waiting for reform to arrive.

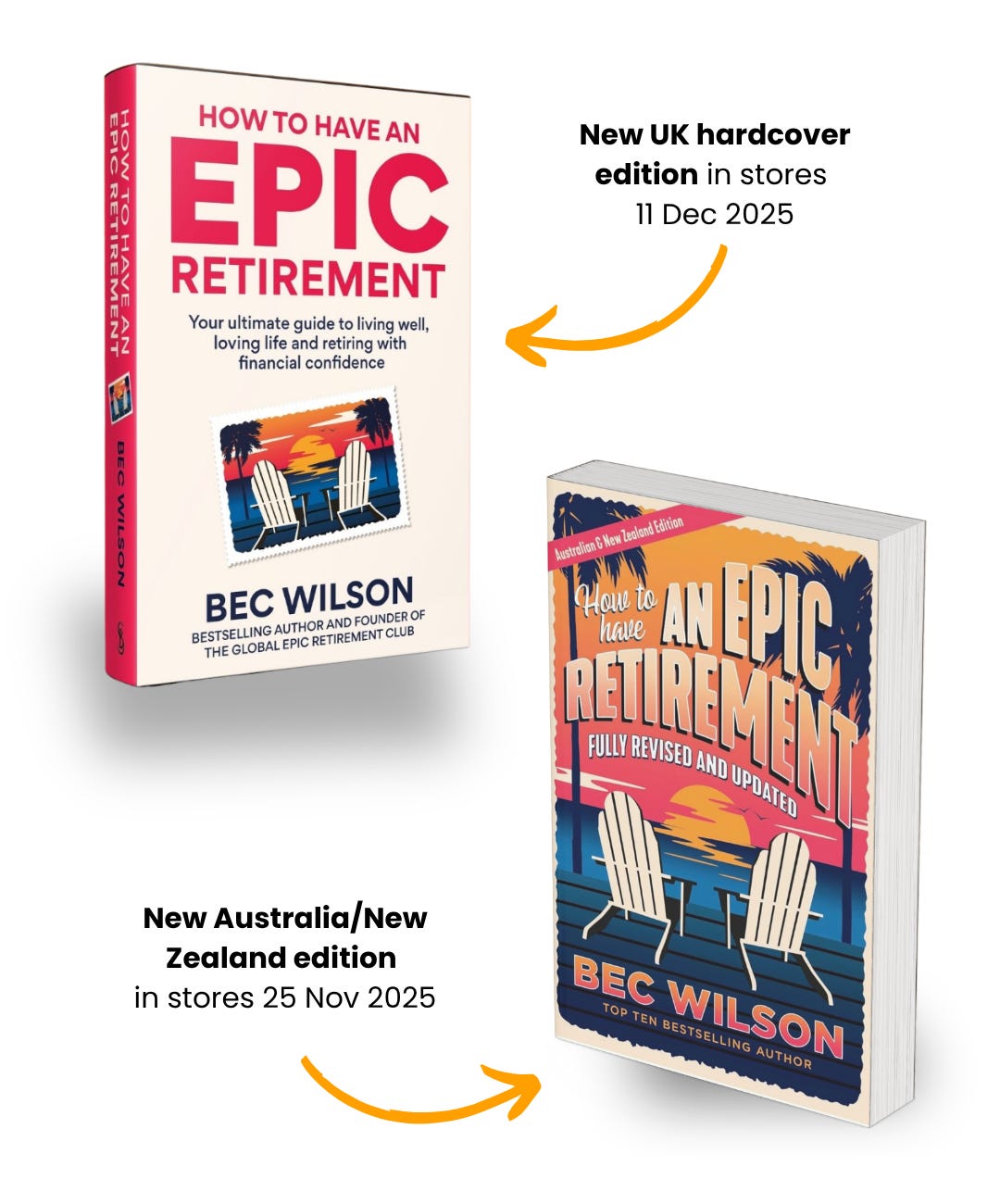

The UK edition of How to Have an Epic Retirement is in its final stages and will hit shelves in December, with the Australia/New Zealand edition arriving just before in November. So it’s shaping up to be a huge end to the year for Epic Retirement.

And while you’re in the mood for small but powerful wins – take ten minutes this weekend to check your pension contributions. It’s one of the simplest ways to get your future self a little closer to an epic retirement.

Until next week,

Make it epic.

Got something to tell me - just reply to this email - or leave a comment here. I’m always looking for article inputs, real stories and questions I can help with answers to.

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

On the UK book…

In case you missed it, I revealed the cover of the UK edition of How to Have an Epic Retirement two weeks ago. It’s a brand-new hardcover, completely rewritten for the UK, packed with detail on the State Pension, workplace and private pensions, and the realities of building a great UK lifestyle. The cover itself is a bit of a showstopper too, very different, and (I’m told) very British!

The book went to print this week and lands in stores on 11 December, which means I’ll soon officially be an author in three countries. (Fingers crossed I get to add bestselling to that line soon!)

👉🏻 You can pre-order your copy now to make sure it arrives before Christmas — see it on Amazon here.

(Important: Make sure you order the Hardcover edition as the other one is the Aussie book)

EDUCATION before leaving school & starting work is what's needed

So many people believe that because 8% is the default amount to go into workplace pensions that it's enough.

Each workplace should also run mandatory pension training, people need to understand their pension statements & know they can increase their contributions.

It's scary how little some people know

Totally agree with other comments regarding education.

I endeavour to educate young people about the power of early investment and compounding. Too many young people are trying to live the millionaire's lifestyle on a shoestring budget and rather than nurturing investments they are fueling debt through "Instagram" pitched photos of flash cars and lifestyles.... All this is eroding potential future wealth as most take loans and get into debt - for a show-off lifestyle?!

People need to get real and not rely on the UK government to support their future selves. This is already causing rifts in the UK where divides are being created and it's got to the point of impacting immigration and foreign investment whilst the country priorities patriotic roundabout paintings.

Education needs to be drilled into young people...invest for your future self as nobody else will prioritise your future wellbeing!