The retirement tool the industry doesn’t want you using (but you already are)

And, in The Times: '‘We had to sell our home’ — the reality of retirement without savings'

In this week’s edition:

Feature story: The retirement tool the industry doesn’t want you using (but you already are)

The Times: ‘We had to sell our home’ — the reality of retirement without savings

From Bec’s Desk: Help me explore whether you’d use an Epic Retirement Tick for UK Workplace Pension funds

The retirement tool the industry doesn’t want you using (but you already are)

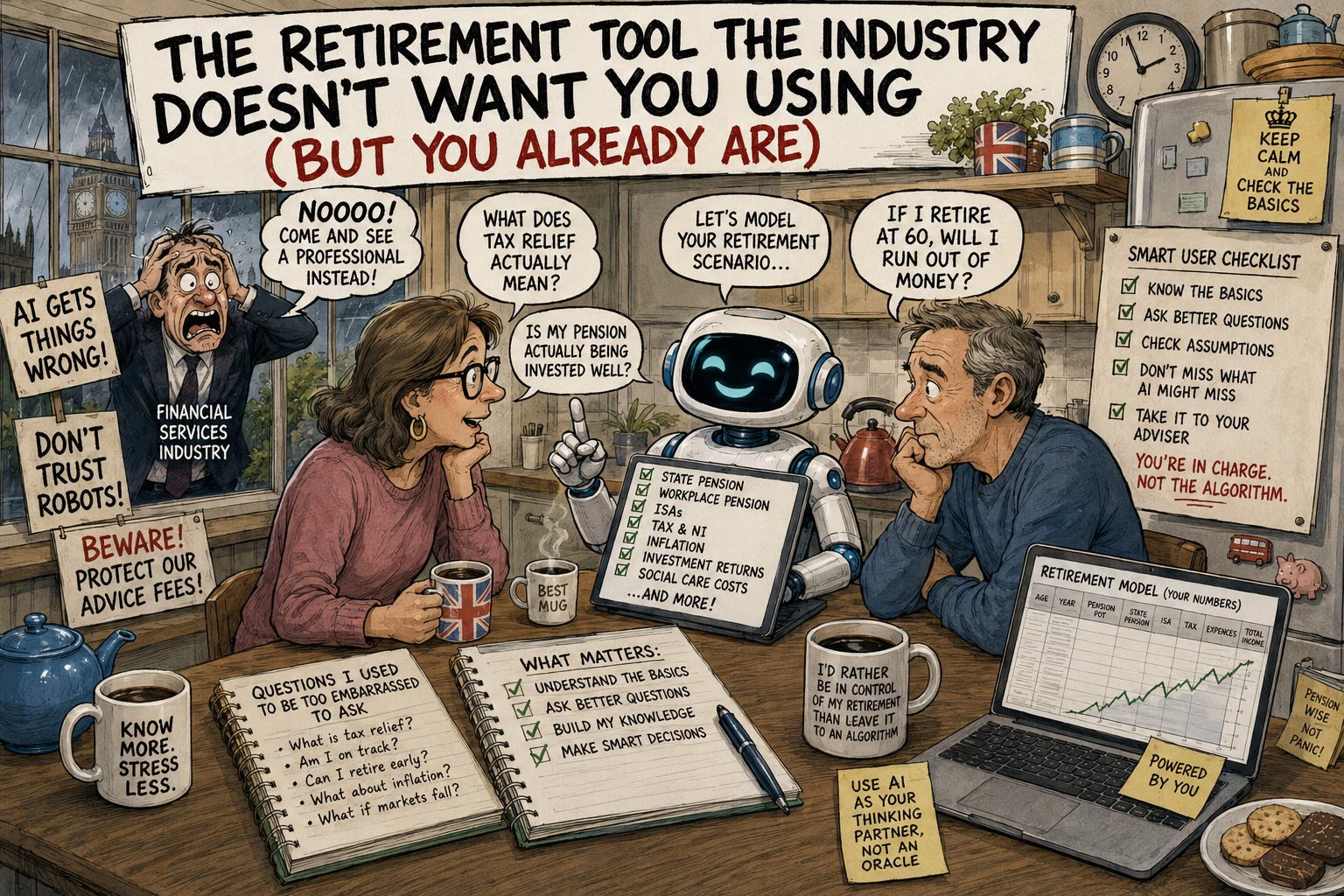

Something is happening at kitchen tables across the UK, and the financial services industry is quite often losing its mind, loudly, about it.

People are asking AI about their retirement. How much money they need, and how to invest, and how to plan for it. They’re even asking Claude to build Excel-style financial models, and it can do that straight from the ordinary chat window, with no special setup needed.

They’re not asking their adviser first, or their pension provider’s helpline, or even their brother-in-law who works in finance and holds court at Christmas. They’re opening up ChatGPT or Claude on their phone and typing the questions they’ve been too embarrassed to ask anyone: What does tax relief actually mean? Is my pension actually being invested well? If I retire at 60, will I run out of money?

Let’s face it - that last question matters and there’s a particular kind of shame that comes with not understanding your own financial situation in your 50s, when you feel like you should have it sorted by now. AI gives people a judgment-free place to start asking questions and building understanding.

And here’s where I part ways with most of the financial industry on this. I love it. The agency it gives you to be curious and consider things from different perspectives is powerful. The fact it can build you a genuinely useful spreadsheet, one you can fill in with your own numbers and take straight to your adviser, is nothing short of fabulous.

The standard adviser response to AI is some version of “be careful, it gets things wrong, come and see a professional instead.” And yes - AI does get things wrong. I catch it out all the time. It uses old data, leaves a critical number like inflation out of a calculation or a spreadsheet, or simply doesn’t grasp the interplay between the State Pension and your workplace pension, ISAs and tax - unless you prompt it to. I push back, ask it to check things, or feed it the correct facts straight from gov.uk, and you need to be aware of those limitations if you use it.

There’s lots of studies being done on this. In one study, it gave incorrect or incomplete answers to about a third of the financial questions it was asked.

So let me be clear. It probably doesn’t know your full picture. And without it, it can’t model your real tax situation, and even with it - I’d be worried you left something out. It has blind spots around things like sequencing risk and social care costs that could actually hurt you if you act on its answers without understanding what’s missing.

But the solution to that isn’t to avoid AI. It’s to know enough that you’re not dangerous when you use it.

Here’s what I mean by that. If you ask AI “will I have enough to retire?” and you don’t know what questions to follow up with - about drawdown rates, about inflation, about what happens if markets fall in your first few years of retirement - you’ll get a confident-sounding answer that might be quietly wrong in ways you won’t spot. AI doesn’t volunteer what it left out. It answers what you asked.

But if you understand the basics? Suddenly you’re having a completely different conversation. You’re the one steering. You’re asking better questions, pushing back when something doesn’t add up, and using AI the way it’s actually meant to be used - as a thinking partner, not an oracle.

That’s always been the whole point of what we do here. Not to replace professional advice, but to give you enough understanding to be a smart consumer of every resource available to you. So that when you talk to your pension provider, you know what to ask. When you see a financial adviser, you understand what they’re telling you. And yes - when you open up Claude at 11pm with a question you’ve been sitting on for months, you know how to make that conversation count.

AI hasn’t changed that mission. It’s just made it more important to learn and know your stuff.

So use the tools and ask the questions you’ve been too embarrassed to ask. Just make sure you’re building the knowledge alongside it, so you’re the one in charge of your retirement decisions, not the algorithm.

I’m smiling ear to ear this week because the mid-course feedback rolling in on our Australian and UK Epic Retirement courses, both running right now, is just so good. I feel incredibly proud of our six-week retirement education program which just keeps getting better.

It’s the main part of what we do here at the Epic Retirement Institute: helping people understand how retirement actually works so they can make better decisions and feel more confident about the future with a 6-week course.

Humour me while I share some of the shorter comments:

“The course is fantastic: so clearly and well structured. Thank you”

“We love this course content and the structure of it - will be recommending it to others!”

“Reallly enjoyed this week. I helped me to understand exactly what I have and what I can do going forward”

“This course has changed my life!!”

“This week I learnt, retirement isn't just about accumulating money. I will need it to support the life I want to live, buy trusting my plan, and allowing myself to spend on things that bring value and enjoyment. I'm still learning and sometimes the numbers say you're fine, but your mindset takes a little longer to catch up.”

“I have been enjoying this course immensely. I feel much more confident in my understanding of how this thing called retirement works!”

“Overall, a very good course, which I wish I could have done a year ago.”

“I loved the phrase that doing wills and funeral planning is an “act of care” and will include that in conversations.”

That’s the kind of confidence I want people to have. And it’s why we choose the projects we do at The Epic Retirement Institute.

In fact, we're contemplating a new project for the UK and I’d love your feedback. We’re considering evaluating workplace pensions as you approach retirement, using a set of clear criteria to assess whether the service and investment options on offer are genuinely good enough, or whether it's time to start asking harder questions. We already run something like this in Australia, called the Epic Retirement Tick that is widely respected by both the industry and everyday people.

It's a full assessment of every fund, not just the ones that come out looking good, and the funds that meet a high enough standard on performance, fees and service earn the Epic Retirement Tick, so you can see at a glance which ones are actually worthy of your trust, and which ones need to work harder. It’s done an amazing job of making retirement performance and services more transparent in Australia and putting pressure on funds to lift their game (And they’re responding in ways only public scrutiny can drive). We think it could do the same in the UK where the first time a lot of people really can contemplate deep strategy on their pensions is in the lead up to and in retirement when your workplaces no longer drive it.

We’re not government-funded consumer advocates or anything, just aware that there’s really no one else in the retirement space who doesn’t make money from selling you a financial product or service, and who can have your education about all the choices available to you as the priority. But we only want to run projects that you’d actually use, so we’d love your feedback. Would you use something like this to review your workplace pensions, and consolidate into the ones that earn the Tick?

Appreciate the honest feedback!

Now, back to your Sunday programming! Our Epic Retirement UK Flagship Course is going so well that we’ll be flipping it into an on-demand program you can access when it suits you to do the course as soon as the Summer program completes. You can register your interest for our full release here. We’ll offer a special deal for those who are pre-registered.

I hope you find time out occasionally too.

Bec Xx

Author, podcast host, columnist, retirement educator, and guest speaker

I am the retirement columnist for The Times, UK. You can read my most recent column here or look through all my columns here.

‘We had to sell our home’ - the reality of retirement without savings

With an estimated 15 million undersaving for later life, many will find they have to make compromises to avoid hardship

Vivian divorced in 1990 and raised her three children with no financial support from their father. She couldn’t afford a private pension, and had almost nothing in workplace savings, despite decades of work, sometimes three jobs at a time just to make ends meet.

She should have retired last year but is working full time on minimum wage to cover her rent and keep her lights on. For her, a comfortable or even modest retirement is a long way from reality. The state pension will be her main source of income.

She is one of the members of my Facebook group, Epic Retirement Club, who shared their experiences this week. In a group full of proactive planners working hard to get ahead and use the systems of retirement to ensure that they will be comfortable, not many were willing to come forward in public and talk about what it feels like to not be on target. But plenty sent in private messages about their plight. It’s tough out there. And many of those who have retired, or who should have retired, are just scraping by.

The conversation came after the latest Retirement Living Standards from the industry body Pensions UK, which set out the estimated incomes needed for comfortable, moderate and minimum lifestyles in retirement - numbers that lay out what it really costs. Last month the government’s Pensions Commission reported that 15 million people in the UK were undersaving for retirement.

The article was published in The Times, on Thursday June 11 and is available for reading here.

Got your copy of How to Have an Epic Retirement - the UK edition yet? Order it now on Amazon here.

Got a topic you’d like me to cover? Send me a message

Simply hit reply and send me a note. I’m keen to know what’s worrying you, what is driving you and what you want more conversation and education about.

Why do I write a separate newsletter for the UK?

I write a separate newsletter specifically for the UK, because the financial system here is completely different to Australia, where I’m based. Your retirement is shaped by the State Pension, workplace pensions, ISAs and HMRC rules. Not superannuation or the Australian Age Pension.

If I just sent you the Australian version with a few words swapped out, it wouldn’t actually be useful to you. And useful is the whole point.

The big conversations, about when to step back from work, what you want the next chapter to look like, how to make your money last, those are universal. But the practical detail needs to reflect the system you’re actually living in. So that’s what we’ve built here. Tell your friends - we want to help you make your retirement epic - the UK way.

Welcome to the UK edition.Thanks for reading Epic Retirement UK! Subscribe for free to receive new posts and support my work.

Interesting piece!

Im a corporate strategist working at a pension insurance giant in the Netherlands. I started to share my thoughts about the financial markets, (geo)political events and, of course, pensions and pension funds. I have some recent articles on pension system and some serious issues with them. You might find it interesting