Retirement for beginners: Where do you begin when you’re thinking of retiring?

Download your Epic Retirement Starter Kit for the UK here today. It's only available during Epic Retirement Month!

In this weeks newsletter:

Feature: Retirement for beginners: Where do you begin when you’re thinking of retiring?

The Times: The five secrets of the happiest pensioners

From Bec’s Desk: 11 days to go

Retirement for beginners: Where do you begin when you’re thinking of retiring?

Every time someone in the UK starts thinking about retirement, the first feeling tends to swing one of two ways. For some, it’s excitement – the long-awaited promise of freedom, travel, hobbies, lie-ins, or simply getting their time back. For others, it’s pure dread. Not loud panic, but that quiet, creeping financial fear that has you instinctively avoiding anything labelled “pension pot”, “State Pension age”, or “drawdown”.

And I see it everywhere. In my Epic Retirement Facebook group, in the Q&A after a talk. In hushed conversations at work. People pull me aside and ask the exact same question:

“How on earth do I know if I’ve got enough to retire?”

It’s a fun number to contemplate. It’s also the wrong first question to start with.

Most people in the UK jump straight into talking about pot sizes, spreadsheets, online calculators and worst-case scenarios. And then they stall. They put off retiring while they wait for the “perfect” number – the magic figure that will suddenly make the whole thing feel safe. Others avoid the topic altogether, hoping that if they don’t look at it, it might somehow sort itself out. It doesn’t.

And in the meantime, many end up chasing someone else’s idea of what a “proper” retirement should look like, only to discover they’ve waited too long. Redundancy gets them, their health shifts or their ageing parents need care and attention and suddenly retirement isn’t a choice anymore – it’s something that happens to them.

But I have to be clear - the starting point for a good retirement isn’t the numbers. It’s much more personal than that. It’s about understanding where you are in life and setting a vision for the years ahead – one you can afford, and one that actually reflects how you want to live in the different stages of your retirement; and what you want to do with your time, health, and best years. And I should point out that I believe retirement shouldn’t be a finish line, but a slower transition. That, in itself, reduces the risks of financial and personal shock. I’m launching a book in the UK next week called How to have an Epic Retirement. Here are some of the steps I walk retirement beginners through.

Think about your goals

Before you even start to dig out your pension statements and hunt for your lost pots, start with some prickly questions. What do you want your mornings to feel like? Where do you want to live? Who do you want around you? Will you work part-time for a bit, switch to consultancy, or walk away from paid work entirely? Do you want to travel and if so, how often and how far from home? Will you be caregiving, and how intense is that role? Will you study, be a volunteer, or learn something new?

Then I want you to go a layer deeper: what does a genuinely great week look like for you? Not a fancy Facebook retirement – consider your real expectations of daily life. The rhythm of your days matters more than you think once the structure of a job disappears.

These are not fluffy lifestyle questions. They are the foundation of your goal-setting, and they must come before the budgeting really kicks off. You simply can’t work out what your future will cost until you know what you want that future to look and feel like. And even the smartest financial adviser can’t set these goals for you (they might try). Only you can do that bit.

Explore how much is enough

Once you’ve mapped out the life you want, then you can start working out what it might cost. And this is where people often discover something surprising: their number is usually far more achievable than they feared.

“How much do I need?” isn’t a single magic figure at all. It depends on four things: the lifestyle you’ve just described and how grand it is; the income you actually need each year to enjoy it; how much comes from your workplace pension, personal pensions, the State Pension and other investments; and finally, your health, longevity expectations and your family responsibilities.

Most people in the UK will draw their retirement income from a mix of workplace pensions, SIPPs, ISAs, cash savings, part-time work and, for just about everyone, the State Pension. That means the big lump-sum question matters far less than people think.

And here’s the bit most people underestimate: over a long retirement, the full new State Pension adds up to a healthy amount – potentially more than £220,000 over twenty years. That’s larger than many people’s private pension pots at retirement.

So the real question isn’t “How big does my pot need to be?” It’s “Do I understand how the different layers of retirement income work together, taxable and non-taxable – and how they’ll change over time?”

Run the numbers – then get some help

If you’ve never run your own “retirement income” calculation before, this is the moment to start. Your pension provider will usually offer a projection either through their app, website or guidance service. You can plug some numbers into a simple online calculator. Then take a breath and think about what kind of advice you might need to give you confidence.

Most workplace pension schemes now offer free or low-cost guidance, and many people don’t realise they already have access to this through their fees. If your needs are simple, this level of guidance may be enough. If things are more complex, you may need regulated financial advice – and if your scheme’s guidance isn’t great, consider that a useful lesson when you eventually merge pots for retirement.

Set up your retirement account and your drawdown

Once you’ve worked out roughly how much income you need, the next piece of the puzzle is understanding how to turn your pension pot into a regular income stream. In the UK, this means thinking carefully about which income source you draw from first, how you manage tax, and how all your pots fit together – workplace pensions, SIPPs, ISAs, cash savings, part-time earnings and any DB benefits you’ll receive.

And here’s the part many people overlook: the order in which you access your pots can have a huge impact on how long your money lasts. Unlike pensions, ISA withdrawals are completely tax-free. Pension withdrawals (beyond the 25 percent tax-free lump sum) are taxed as income. So choosing when to draw from each can help you smooth your tax bill, stay out of higher tax brackets, or even delay triggering the Money Purchase Annual Allowance if you want to keep working and contributing.

If you have a defined benefit pension, that adds another layer. Your DB income often acts as a guaranteed underpin for your essential spending, which means you may be able to take more investment risk with your DC pension, hold onto it for longer, or draw from your ISA first to keep your tax bill down. Understanding how these pieces sit together is just as important as knowing the size of the pot itself.

This is the moment where planning becomes reality. Drawing money from your pension isn’t just a tap you turn on; it’s a long-term tax strategy. You need to think about how much to withdraw, how often, how your withdrawals interact with any work income, and how you’ll invest the remaining balance so it continues to grow and support you over decades.

Spend too quickly and you risk running out. Spend too slowly and you risk reaching your later years with a pot you never enjoyed, and under the new rules, the last surviving partner may hand 40 percent of whatever’s left straight to the taxman. That’s a harsh penalty for being overly cautious.

And finally, dig in on your sense of purpose

Ultimately, the reason you set up your finances is to give yourself the freedom to spend your time on things that energise you. These are things you choose, regardless of whether they pay. And that shift can be surprisingly confronting.

So many of us tie our identity to work. Stepping away from a job title or a role can leave a bit of an identity vacuum until you consciously refill it. Taking the time to think about what you value, how you want to contribute, and what makes you feel connected is an essential part of the transition.

Your purpose doesn’t need to be grand or fancy. It just needs to be something you’re going to seek actively.

Which brings me back to this time of year

The end of the year is when many people in the UK quietly step out of the workforce. Some have been planning the transition for years. Others get nudged there by restructures, health shifts, or caring responsibilities. And with rising workplace pressures and a huge cohort reaching their mid- and late-60s, we’ll likely see a big wave of retirements this winter.

So if you’re thinking about retiring between now and the new year, start with the basics. I’ve released a free starter kit – a simple toolkit to help you map out some goals, think through how much is enough, and consider your sense of purpose. It’s a great place to begin.

And remember: retirement isn’t a finish line. It’s a long, gradual shift into a different rhythm of living and earning. The more prepared you are going in, the easier it is to make good decisions and avoid the traps that catch people who leave it too late.

It’s Epic Retirement Month!

20 November to 20 December is Epic Retirement Month. It’s the time of year when the largest number of people retire across the western world, based on my own insights and data – and it’s a moment worth supporting.

So we’re rolling out thirty days of inspiration, education and the kind of practical advice that helps you shape the second half of life on your own terms.

If you’d like to dive deeper, visit my new website: www.epicretirement.net

And in the month ahead comes one of the biggest moments of all: the launch of the completely new UK edition of How to Have an Epic Retirement.

And, over on my website we’ve released The Epic Retirement Starter Kit - a free 16 page guide to help you navigate retirement - with a dedicated UK edition. It’s just for Epic Retirement Month. Go get it!

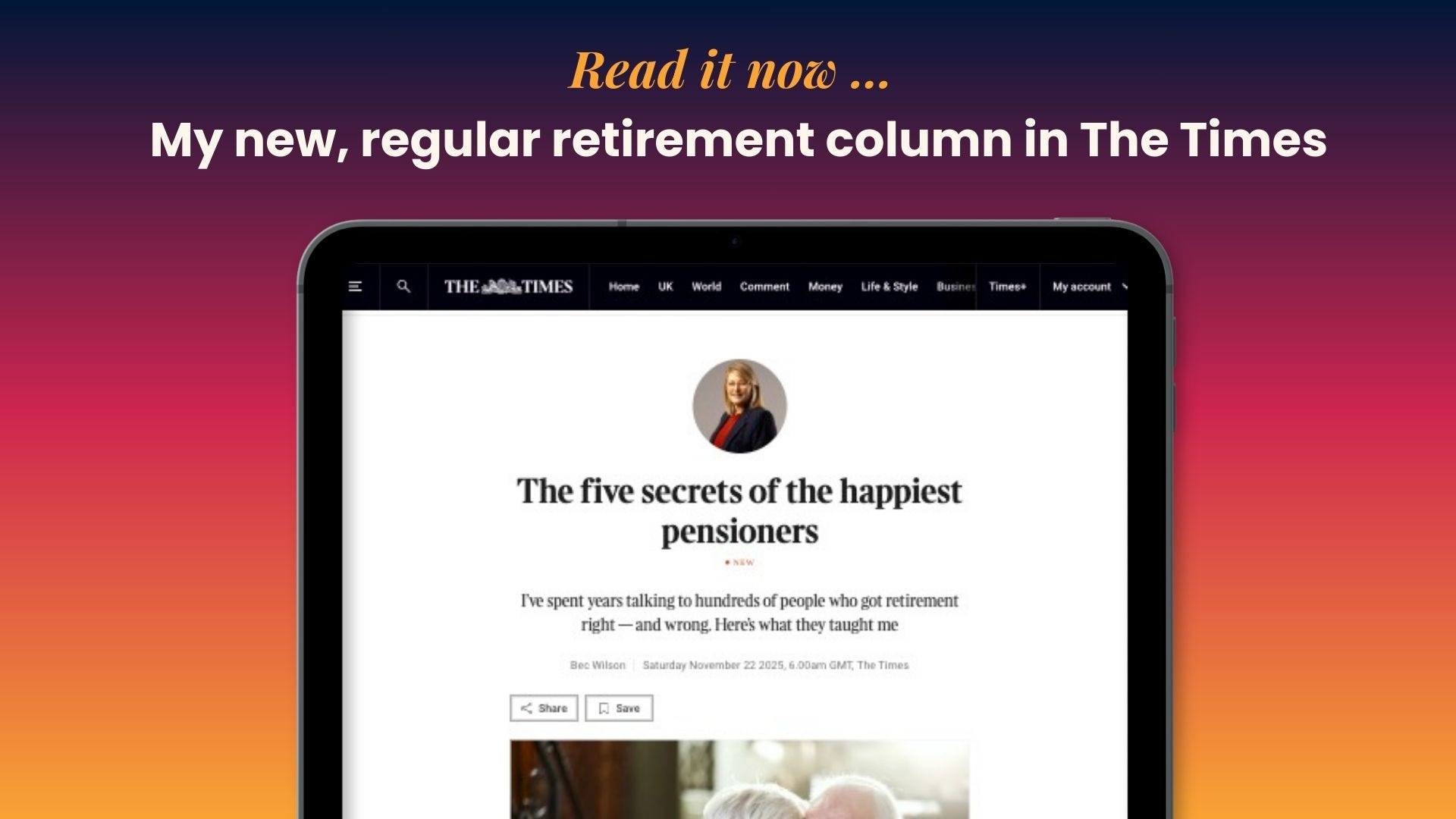

If you missed my debut column in The Times and Sunday Times, you can read it here.

The five secrets of the happiest pensioners

This article, my new regular column, appeared in print and digital in The Times new Consumer Money section on Saturday 22nd November.

It’s not enough just to retire in this day and age — expectations of retirement are much higher than that. UK life expectancy now means that one in four 65-year-old men will live to 92 while one in four women will live to be 94. The goal isn’t simply to retire comfortably; we’re under more pressure than ever to retire happily.

Let’s face it, retirement is one of the most complex financial challenges of our time. We plan for it thinking that it’s about money and stopping work. But it’s so much more. It’s about using what you have, to build a life powered by passive income — one that brings you purpose and joy for 25 to 35 years, step by step.

After years of talking with hundreds of people who have managed to get this stage of life right, along with plenty who haven’t, I’ve come to see a clear pattern. People often ask me for the secrets of the happiest people in retirement — and I can boil it down to five valuable lessons.

Do the financial groundwork

The happiest pensioners I see have financial sensibility and excellent money habits. They saved consciously for retirement, paid off their mortgage and moved out of the rat race with a plan, usually on a timeline that they have been able to shape. They built multiple income streams, from pensions to Isas, dividends or part-time work, and they understand how those pieces fit together.

They are financially literate and engaged with what they have and what it can do for them, not in a spreadsheet-obsessive way, but in a confident, capable one. They understand tax-efficient contributions, the value of compound investing, the importance of growth assets, and how to turn their money into an income that suits their retirement lifestyle goals.

Focus on cash flow, not pot size

Happy pensioners aren’t fixated on how big their savings pot or pots are; they are focused on how their money flows. They know when and where income arrives, how long it lasts, and what it can support. They understand how to minimise the tax on that income, and how to pull in their belt in a tough year.

This article is a full feature which continues in The Times - you can read it here.

I'm really counting down now.

I received a special delivery this week from the UK. It was my first sighting of the UK book. And I have to say it’s beautiful. This is the first time my book has been produced in a hardcover edition, and the matt finish with gloss touches on the Epic Retirement elements gives it a very premium feeling that no photograph conveys. Neevertheless - I’ll share some photos.

You can share in my unboxing moment - I filmed a reel for Facebook!

Just 11 days to go now - so do get your order in if you haven’t already.

You can order it on Amazon now if you’d like to make sure you receive your copy in time for the holidays.

As you might have already seen, my first column went live in The Times in the UK last weekend: “The secrets of the happiest pensioners.” I’m their new retirement columnist, and it ran as a full Saturday feature. If you have a read, let me know if it resonates — and please send through any ideas or questions you’d love me to tackle in future columns. Retirement education travels well.

Finally, I’ve been posting regular reels on Facebook, and I’m starting to incorporate UK reels in the mix. I’m having a lot of fun providing retirement education you can trust. You can follow along at facebook.com/becwilsonepic or on Instagram at instagram.com/epicretirement.

Hope your Sunday isn’t too chilly… until next week - Make it epic!

Bec x

Author, columnist, retirement educator, and guest speaker

How to Have an Epic Retirement: Your ultimate guide to living well, loving life and retiring with financial confidence

If you’ve ever wondered what your own epic retirement could look like, this book is for you. How to Have an Epic Retirement guides readers through the way the systems of retirement work, so you can learn the valuable lessons that modern retirees wish someone had shared with them before they kicked off the changes and stages of life that come after retirement.

I’d love it if you pre-ordered - it makes a huge difference when retailers can see early demand for the book - they then get actively behind it.

🔷 Order it on Amazon here. 🔷 The book is a hardcover only in the UK so please don’t order the paperback - (the paperback is linking to the aussie/nz export version).

Very good information!

I NEVER WANTED TO RETIRE!

I'm one of those lucky people who's always done what they enjoy doing, or I wouldn't do it. For that reason, I never really wanted to retire in the traditional way.

I was in the first round of COVID-19, and I caught it really badly. I didn't just have a headache; I had it for seven weeks, and I think I had just about every symptom except the respiratory symptom of COVID.

After I began to get better, I'd lost my balance. My body got weak and needed rebuilding, but I'd lost my balance, and it's never properly returned. That changed everything.

Also, it seemed to clear my mind and brain of the past 40 years of thoughts and ideas, as if I had a new slate and started thinking about things from day one again.

I started with a notebook, writing, Recording and Exploring what I wanted from life. I had two columns:

- What I don't want

- What I want

One of the things I definitely didn't want, living in the UK, was the cold, the dull, the winters. I've never enjoyed them, not for a moment. What I wanted was year-round sunshine. I wanted to live life on my terms, and for me that possibility was a little bit easier. You see, I have a Philippine wife.

Since that time, I've spent eight months of the year in the colder UK, living in Cebu. It's wonderful, and I have a very active life and I'm achieving my goals every day.

I would advise anyone not to think of retirement as giving up and starting a new life, but as having the opportunity to do more of what they want. Don't become sedentary and sit down. I have no choice, because I can't stand that long, but I keep my Pain. very, very active, and I am having a fantastic retirement.

Just remember, whatever it is you want, there is a solution and a way of getting it. In fact, there are many ways; you just have to discover them.

It starts with a notepad and a pencil and you writing them down, because when you write them down, you've started the commitment. You start thinking about them, and if you go back to those thoughts every day, those desires, and write a little bit more, and ask yourself lots of questions, you'll move toward achieving them. You really will!

I would love to speak more on this subject. If there is anything you want to know, or if you have any ideas or things you think I should answer, please comment.