New data out: What does a comfortable retirement cost now?

And, in The Times: 'Your pension is primed to let you down at the worst possible time'

In this week’s edition:

Feature story: New data out: What does a comfortable retirement cost now?

The Times: Your pension is primed to let you down at the worst possible time

From Bec’s Desk: Winter down under - UK course in Week 2

New data out: What does a comfortable retirement cost now?

Pensions UK just released its annual Retirement Living Standards and for the first time in a few years, the picture is a little more nuanced than “everything went up again.”

Phew - I hear a few of you thinking out loud.

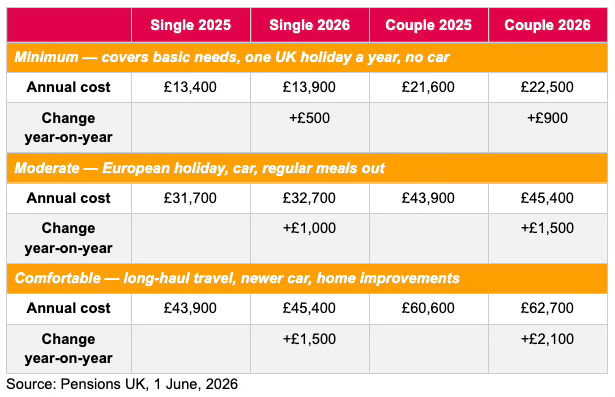

The Standards describe three retirement lifestyles: Minimum, Moderate, and Comfortable. Each one is built from detailed research into what people actually spend in the uk on life and living it - food, transport, holidays, energy bills, eating out. They’re updated every year, and the 2026 figures have just landed this week.

Here’s where things stand, and how they’ve moved:

Pensions UK Retirement Living Standards 2026

Note: these are after-tax spending figures. The gross income you’ll need to generate them will be higher, depending on your tax position.

The comfortable standard for a single person has risen by £1,500 in a year. For a couple, it’s now £62,700, up from £60,600. The increases at the moderate and comfortable levels are being driven by inflation across various spending categories, including things like rail fares, which rose sharply enough that the annual rail budget in the research jumped from £100 to £180 per person.

The minimum crept up only modestly - £500 for a single person - because it's a stripped-back budget with limited discretionary spending. The bigger jumps are at moderate and comfortable, where the things people actually want in retirement - travel, eating out, leisure, and lifestyle have all kept getting more expensive.

We need to think about these standards alongside the State Pension

The full State Pension is currently £12,548 a year. For a single person, that almost covers the Minimum standard (£13,900) - there’s a gap of about £1,350 to find from elsewhere.

But the real story is in the middle tiers. A moderate retirement for one person costs £32,700. That means you need roughly £20,000 a year on top of the State Pension. A comfortable retirement requires over £32,000 a year on top.

That’s not pocket money. For a single person targeting comfortable, using the standard 4% drawdown rule, you’re looking at a pension pot in the region of £800,000 - on top of whatever State Pension you receive.

For couples the numbers are more forgiving. Two State Pensions combined come to around £25,000 — which covers the Minimum comfortably and gets you halfway to Moderate. But a comfortable retirement for two still needs nearly £38,000 a year from savings and pensions.

What this means for most people, practically

Three things are worth taking from these numbers.

First, the comfortable standard isn’t THAT extravagant. It includes long-haul travel once in a while, a car, home improvements, and being able to help family occasionally. It’s a normal, full life - not a luxury one. The fact it now requires £45,400 for a single person is a reflection of what ordinary things cost, not high standards of living.

Second, the gap between where most people will land and where they want to be is often larger than they expect. The State Pension is a solid foundation, but it was never designed to do the whole job.

Third, these figures assume you own your home outright. Mortgage payments or rent are not included. If you’re still carrying housing costs into retirement, your real number is higher.

None of this is meant to alarm you! It’s meant to ground you. The point of these benchmarks is to give you something real to plan against, rather than you just sitting with a vague aspiration to have a good retirement. Pick the lifestyle that feels right for you, work out your gap, and start there.

Or even better - write your own budget. That’s really the best way to do retirement planning.

Winter arrived this week down under where I live. Not a British winter by any standard though. It was chilly ( mild 12 degrees in the mornings), windy and sunny… delightful. It’s the sort of weather that makes you want to walk outdoors and feel the sun on your face. And so I have, every - single - day. With no travel for a few weeks, I’m delighting in getting through the workload on my desk, rebuilding my website, supporting the courses currently underway in the UK and Australia; and preparing for the launch of the next programs.

I’ve also signed my next book deal - a fun project to get started on. And this time I’ve gone with Penguin Random House as the publisher - a big change for me. When I wrote my first retirement book only one publisher was curious - all the others said there’s no market for this stuff. ☺️ Three years later I had a few wanting a piece! Must be doing something right. I’ll tell you more about the 2 book deal I’ve signed on for once the books take shape.

Our Epic Retirement Courses are going great guns. In the UK, we host our first live Q&A - cant wait to get up at 3am for that to see everyone. Our first students are keenly working through the course, that is now up to week 2. And the feedback is superb!

“I love the videos and the reflective activities. The layering concept was a really good way to describe funding a retirement.”

“The presentation of even the tough topics is very good, and the format is fantastic. Now that I'm into the course, I just want to keep going. And thank you for acknowledging anxiety levels may rise at times!”

“The course flows at the right pace (for me anyway). Building up some foundational concepts, before diving into more detail with practical examples and comparison points. The reassurance regarding "pot size" vs the lifestyle you want/need is helpful as people (myself included) can be more fixated on a number rather than working backwards”

“This is a brilliant course that everyone should do”

It’s a six week program, and there’s three live events during the program too. There’s still time to join the course. Just book your place and jump straight in. You haven’t missed anything you can’t catch up on with 2-3 hours of on-demand online course-watching, especially if you get in before this week’s live event. Here’s the brochure if you want to learn more about it. And book your place and get started here.

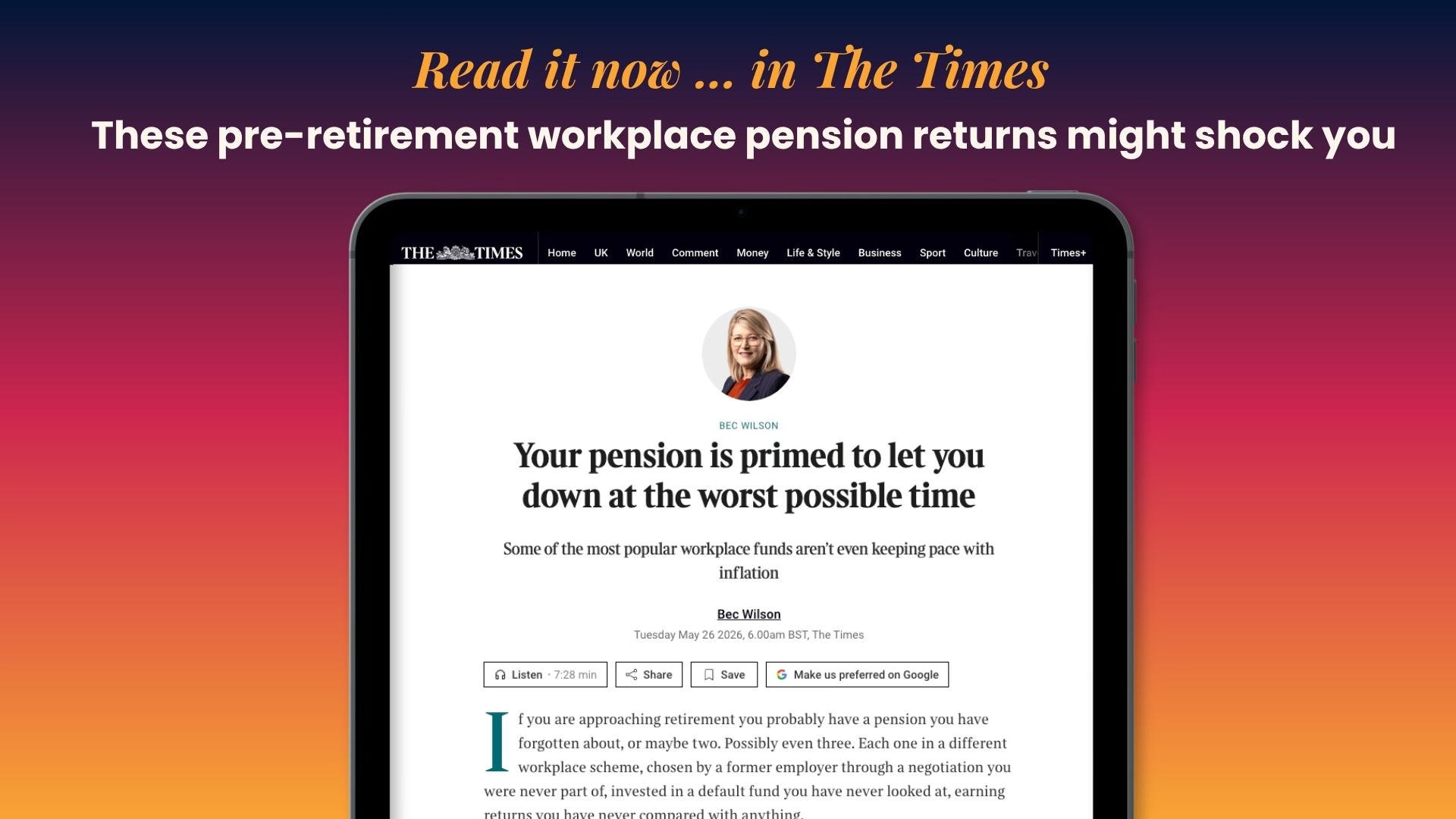

Lastly,I was thrilled to see my column for The Times showed up in the newspaper last Sunday in style. A full half-page! If you haven’t looked at how your workplace pension is performing, I hope I’m inspiring you to, and giving you some useful benchmarks to help you consider whether it’s performing well, or underdelivering. This is important stuff in the years running up to retirement.

Have a read if you haven’t already. And do something about it. This is your retirement - you’ll never regret taking responsibility for making it epic.

Now get out there and make your Sunday epic too.

Bec Xx

Author, podcast host, columnist, retirement educator, and guest speaker

Why do I write a separate newsletter for the UK?

I write a separate newsletter specifically for the UK, because the financial system here is completely different to Australia, where I’m based. Your retirement is shaped by the State Pension, workplace pensions, ISAs and HMRC rules. Not superannuation or the Australian Age Pension.

If I just sent you the Australian version with a few words swapped out, it wouldn’t actually be useful to you. And useful is the whole point.

The big conversations, about when to step back from work, what you want the next chapter to look like, how to make your money last, those are universal. But the practical detail needs to reflect the system you’re actually living in. So that’s what we’ve built here. Tell your friends - we want to help you make your retirement epic - the UK way.

Welcome to the UK edition.

I am the retirement columnist for The Times, UK. You can read my most recent column here.

Your pension is primed to let you down at the worst possible time

If you are approaching retirement you probably have a pension you have forgotten about, or maybe two. Possibly even three. Each one in a different workplace scheme, chosen by a former employer through a negotiation you were never part of, invested in a default fund you have never looked at, earning returns you have never compared with anything.

The system was clearly not designed to help you find out about, or monitor performance. If it had been there is no way the dreadful figures on pension performance in the five years to retirement would have been allowed to stand.

The analyst CAPAdata tracks the performance of UK workplace pension default funds and its figures show what has been happening to workers’ pension returns in the five critical years before they reach state pension age, known as pre-retirement. This is when the stakes are highest and there is little time to recover from a bad decision.

A pension pot at retirement still needs to last another 20 to 30 years, though, which means growth still matters enormously. I have spent years writing about retirement planning, and these numbers are worse than I expected for a period when global markets were delivering some of their strongest returns in decades. They should alarm anyone who has a pension in this country.

The best performing pre-retirement fund in the data set over the five years to March 2026 was the SEI Flexi Default, growing at a compound annual rate of 9.5 per cent - impressive. The worst was Scottish Widows, at a miserable 3.3 per cent a year, a rate that did not even keep pace with inflation.

The article was published in The Times, and is available for reading here.

Got your copy of How to Have an Epic Retirement - the UK edition yet? Buy now on Amazon

Thanks for the article. It helps me plan better for the future. You mention at the beginning that the values are before tax, but all your calculations, like for the 800,000 drawdown example assume there is no take to be paid. A single person will need a lot more than 800,000 saved to achieve the comfortable target once tax is taken into account.